-A Practical Guide for Smarter Business Decisions

Understanding the break-even point and cost behavior is essential for making smarter, data-driven business decisions in today’s competitive environment. Break-even analysis—also known as Cost Volume Profit (CVP) analysis—helps managers, entrepreneurs, and business owners determine the minimum sales volume required to cover fixed and variable costs, assess profitability, control expenses, set optimal pricing, and evaluate new projects with confidence. By explaining break-even formulas in units and sales revenue, real-world business examples, contribution margin concepts, and the practical relationship between fixed costs and variable costs, this guide provides a clear and practical framework for managerial accounting, financial planning, risk assessment, and strategic decision-making. When combined with a solid understanding of cost behavior, break-even analysis becomes a powerful financial tool for improving profit planning, cost control, and long-term business sustainability.

Every business—small or large—runs on decisions. Whether it’s setting the right price, planning production, or evaluating a new project, managers constantly face choices that impact profit. To make those decisions confidently, they rely on powerful financial tools. Among these, Break-Even Analysis and Cost Behavior Analysis remain two of the most practical and widely used techniques in managerial accounting.

What Is the Break-Even Point?

The Break-Even Point (BEP) is the stage where a business makes no profit and no loss. At this level, total revenue equals total cost.

It answers a key question every business must ask:

“How much do I need to sell to cover all my costs?”

Knowing the break-even point gives managers a minimum target to remain financially safe. Anything sold beyond this point becomes profit.

Why Break-Even Analysis Matters for Decision Making

Break-even analysis is much more than just a mathematical formula—it acts like a financial compass for managers. Here’s how:

1. Helps Set the Right Price

Managers can see how different prices affect profitability and find the ideal price point without hurting demand.

2. Supports Cost-Control Efforts

A high break-even point may signal rising costs. This gives management a chance to adjust production processes or negotiate supplier rates.

3. Evaluates New Projects

Before launching a product or service, companies calculate the break-even point to estimate whether the idea is financially feasible.

4. Measures Risk

Industries with uncertain demand—like retail or manufacturing—depend heavily on break-even analysis to foresee revenues under different sales volumes.

5. Guides Strategic Planning

Whether it’s expansion, automation, or adding new equipment, break-even figures help in making informed long-term decisions.

Break Even Point Calculator

A Simple Story: How a Business Owner Uses Break-Even Analysis

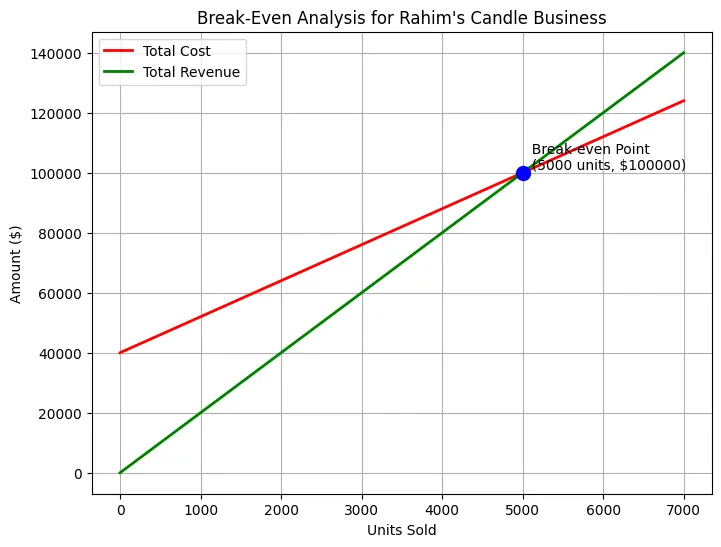

Imagine a small entrepreneur, Rahim, who plans to start selling premium handmade candles. He wants to know how many candles he must sell to avoid loss. He pays fixed amount of rent, rates and taxes monthly basis.

- Selling Price per candle (SP): $20

- Variable Cost per candle (VC): $12

- Monthly Fixed Costs: $40,000

Rahim first calculates the contribution margin: Contribution per Unit=20−12=8\text{Contribution per Unit} = 20 – 12 = 8Contribution per Unit=20−12=8

Break-even units:

40,000÷8=5,000 units40,000 \div 8 = 5,000 \text{ units}40,000÷8=5,000 units

This means Rahim must sell 5,000 candles per month to cover all costs.

Break-even revenue:

Contribution Margin Ratio: 820=0.40\frac{8}{20} = 0.40208=0.40 Break-Even Revenue=40,0000.40=100,000\text{Break-Even Revenue} = \frac{40,000}{0.40} = 100,000Break-Even Revenue=0.4040,000=100,000

Rahim now knows he needs $100,000 in monthly sales just to break even.

Anything above this turns into profit.

This simple calculation gives him clarity and confidence, helping him decide whether to proceed, adjust price, or reduce costs. This is exactly why break-even analysis is such a valuable managerial tool.

Understanding Cost Behavior: Variable vs Fixed Costs

Cost behavior refers to how costs change (or don’t change) when production levels shift.

A common misconception is:

“Variable cost varies per unit and fixed cost is constant per unit.”

This is incorrect. Here’s the real picture:

✔ Variable Costs – Constant Per Unit, Change in Total

Variable cost per unit is usually constant, but total variable cost changes with production volume.

Example:

Material cost of $5 per unit →

- 1 unit = $5

- 100 units = $500

- 1,000 units = $5,000

So variable cost is named for how the total cost varies, not the unit cost.

✔ Fixed Costs – Constant in Total, Change Per Unit

Fixed costs (rent, salaries, insurance) stay the same in total, even if production changes.

But fixed cost per unit decreases as more units are produced.

Example:

Fixed monthly rent = $10,000

- Produce 100 units → $100 per unit

- Produce 1,000 units → $10 per unit

- Produce 10,000 units → $1 per unit

Thus, fixed cost per unit is not constant.

Why Understanding Cost Behavior Is Crucial

Knowing which costs change and which remain stable helps managers:

- Prepare flexible budgets

- Estimate profits accurately

- Set competitive pricing

- Plan capacity and resources

- Avoid misinterpretation of financial statements

Together, break-even analysis and cost behavior insights form a strong foundation for managerial decision making.

Final Thoughts

Break-even analysis provides a clear financial picture of how sales, costs, and profits interact. When combined with a solid understanding of cost behavior, managers can make smarter, data-driven decisions that reduce risk and increase profitability.

In a world where competition grows every day, these tools act as a guiding light for business owners looking to maintain stability and achieve sustainable growth.

Written by Md Kollol Hossain, CEO, CapitalinsightBD — empowering professionals with clarity in finance, analytics, and business strategy.

This article is for educational purposes only and does not constitute financial or investment advice.